2025 Global and China Automotive Components Industry Overview and Development Trends

Categories: News Center

Categories: Industry News

Time of issue:2025-07-30 09:03

(1) Overview of the Global Automotive Components Industry

As the automotive industry market continues to grow, the supporting automotive components market has also entered a mature phase, with distinct regional characteristics in its industrial layout. Internationally renowned automotive parts manufacturers are primarily concentrated in North America, East Asia, and Europe.

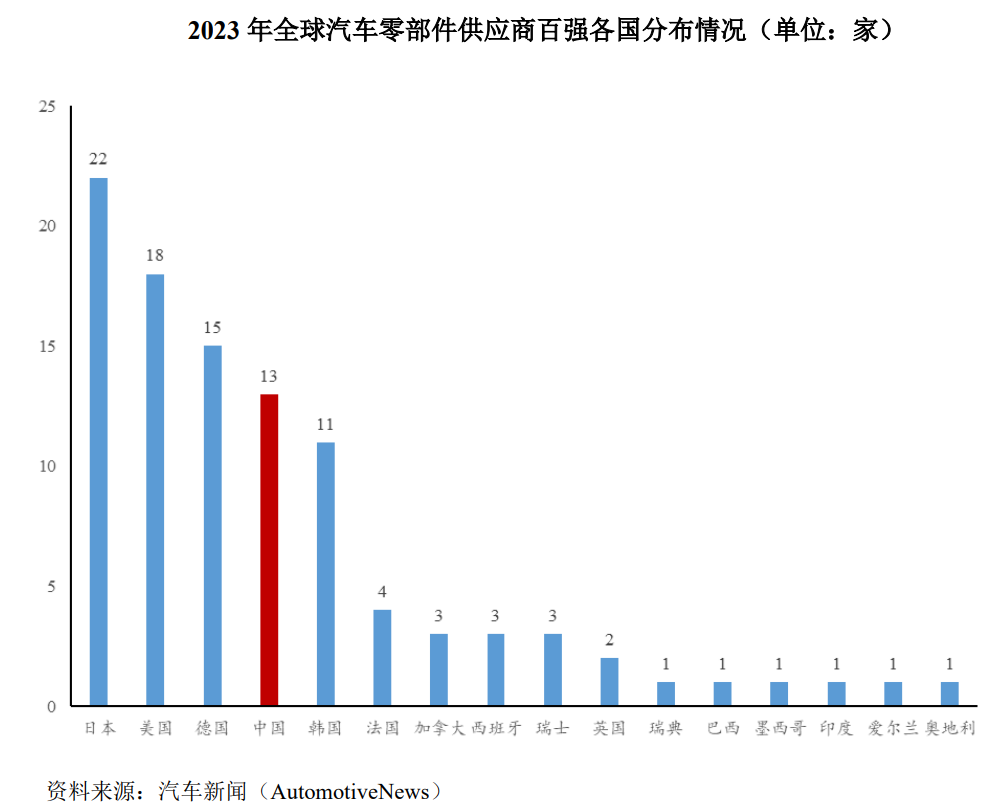

According to the 2023 Global Top 100 Automotive Parts Suppliers ranking published by U.S. publication Automotive News, Japan, U.S., Germany The traditional dominance of major automotive parts countries remains stable, with Japan and the U.S. ranking first and second, respectively, boasting 22 and 18 companies. Germany ranks third globally with 15 enterprises. China’s auto parts industry started relatively late, but after persistent efforts to catch up, it has achieved remarkable progress, securing fourth place worldwide with 13 companies.

(2) Overview of China's Automotive Parts Industry

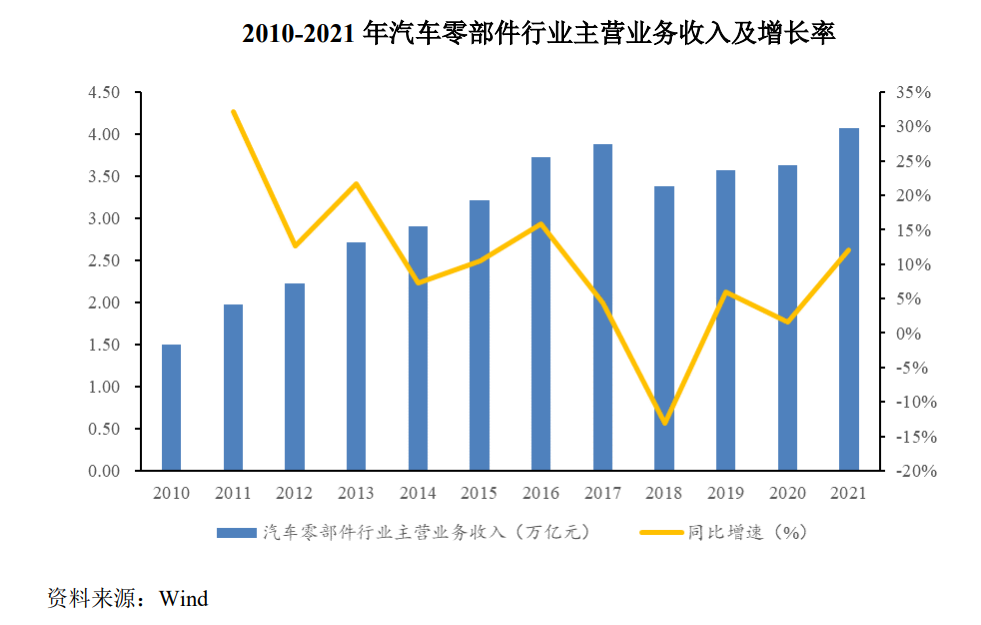

China's downstream vehicle industry has experienced rapid growth, driving the steady expansion of its automotive components sector. According to Wind data, from 2010 to 2017, China's component industry saw continuous growth in main business revenue, rising from 1.50 trillion yuan to 3.88 trillion yuan, with a compound annual growth rate of 14.58%.

Due to the downturn in the downstream vehicle market, the automotive components industry experienced a decline in revenue. In 2018, the industry's main business income stood at 3.37 trillion yuan, representing a year-on-year decrease of 13.04%. However, starting from 2019, revenue gradually rebounded, reaching 3.58 trillion yuan in 2019, 3.63 trillion yuan in 2020, and 4.07 trillion yuan in 2021—corresponding to year-on-year growth rates of 5.98%, 1.55%, and 12.00%, respectively. This marked a clear reversal of the previous downward trend.

Against the backdrop of the globalization of the automotive industry chain, China's auto parts export market is showing a growth trend. According to Wind data, from 2015 to 2023, China's auto parts exports increased from US$46.815 billion to US$87.661 billion, with an average annual compound growth rate of 8.16%.

Affected by factors such as the global decline in automobile production and sales, as well as escalating China-U.S. trade tensions, China's auto parts exports fell 3.60% year-on-year in 2019. In 2020, both supply and demand in the global automotive industry were significantly impacted, leading to a gap in the supply capacity of overseas auto parts manufacturers. However, rising overseas demand helped boost domestic auto parts exports, resulting in rapid growth. In 2020, China's auto parts exports reached US$56.516 billion, representing an increase of 6.55%.

In 2021, the global automotive industry continued to feel the impact of disruptions in overseas auto supply chains. Meanwhile, the rapid growth of the new-energy vehicle market boosted demand for automotive components, driving China's auto parts exports to reach US$75.568 billion—a 33.71% increase. In 2022 and 2023, China's auto parts export values climbed further to RMB 81.089 billion and RMB 87.661 billion, respectively, representing growth rates of 7.31% and 8.10%. Driven by advancements in new-energy and intelligent technologies, China's automotive industry is undergoing a structural upgrade, enhancing its global market competitiveness year after year.

(3) Industry Development Trends

① Increased industry concentration

The automotive parts industry boasts a vast market, numerous niche segments, and a wide variety of product types, resulting in relatively low industry concentration. However, as the industry undergoes structural adjustments, market concentration is showing an upward trend. This is partly due to the global shift in industrial chains, where leading companies from developed countries—such as Europe, the U.S., and Japan—are optimizing their business strategies by gradually divesting from low-tech, low-margin product lines, thereby driving consolidation within the industry.

On the other hand, in emerging markets represented by China, several leading enterprises in the automotive trim industry are gradually realizing economies of scale and have achieved breakthroughs in key core technologies, giving them strong competitive advantages and enabling them to steadily expand their market share. Moreover, taking China as an example, the continuous introduction of new industry standards such as the "China VI Emission Standards" is driving industry upgrades, phasing out a number of outdated production capacity companies and fostering greater industry consolidation.

② The "Four Modernizations" trend is strengthening

Due to trends in the automotive industry such as electrification, connectivity, intelligentization, and sharing, the structure of the automotive components sector has also undergone adjustments and upgrades. Key components for smart connected vehicles—such as advanced driver-assistance systems, vehicle-to-everything (V2X) devices, and LiDAR—along with core parts for new-energy vehicles like power batteries and motor-electric control systems, are gradually becoming the industry's flagship products. According to data from the China Association of Automobile Manufacturers, China is expected to achieve automated driving in low-speed driving and parking scenarios between 2020 and 2025, with the potential for autonomous driving in more complex situations emerging from 2025 to 2030. By 2040, it’s projected that three-quarters of all vehicles on the road will be equipped with intelligent driving capabilities.

③ Rise of Domestic Brand Supply Chains

Domestic substitution is accelerating, particularly in areas such as chips and high-end materials. "Made in China 2025" Policy support is driving technological upgrades among domestic enterprises, enabling some companies to join international supply chains such as those of Tesla and Volkswagen. In 2023, the number of Chinese companies featured in the Global Top 100 Automotive Parts Suppliers increased to 13, with industry leaders like CATL and Gotion High-Tech securing prominent positions. (Source: Sino Insight Research Institute)

Tel: 021-50326815

Email: info@junyi-auto.com

Address: 885 Zhangjing Road, Dongjing Town, Songjiang District, Shanghai